What USDC payroll means for global teams

USDC payroll refers to the process of paying employees or contractors using USD Coin, a stablecoin pegged to the US dollar. Unlike volatile cryptocurrencies such as Bitcoin or Ethereum, USDC is designed for predictability. Each token is backed 1:1 with US dollars held in segregated accounts with US-regulated financial institutions, providing a stable unit of account for cross-border compensation.

This stability distinguishes USDC payroll from general crypto payroll. When a company sends USDC, the employee receives a dollar-pegged asset. Any conversion to local currency happens at the employee’s end, typically on a regulated exchange. This structure allows organizations to maintain consistent payroll budgets without exposing compensation to the market fluctuations inherent in other digital assets.

For compliance and financial planning, this predictability is essential. Companies can model payroll costs in US dollars with precision, while employees retain the option to convert funds into their local fiat currency. This approach balances the speed and low cost of blockchain settlement with the regulatory clarity required for global employment.

Comparing USDC payroll providers and rails

Selecting a USDC payroll provider requires evaluating infrastructure against regulatory exposure and operational cost. The market is divided between native stablecoin issuers, specialized payroll rails, and legacy compliance platforms. Each model carries distinct implications for tax reporting, audit trails, and settlement finality.

Infrastructure and Compliance Models

Circle provides the underlying liquidity and compliance infrastructure for USDC but does not directly manage employer payroll workflows. Its role is primarily that of a reserve manager and issuer, ensuring the stablecoin remains pegged to the US dollar through segregated, regulated financial institutions. Employers using Circle’s infrastructure typically rely on third-party payroll processors to handle the distribution layer.

Rise and Toku operate as specialized payroll rails designed specifically for crypto compensation. These platforms integrate directly with USDC on supported blockchains, offering tools for bulk payouts, contractor onboarding, and automated tax documentation. They bridge the gap between on-chain settlement and off-chain compliance requirements, such as 1099-NEC reporting for US-based contractors.

Bitwage represents a hybrid approach, allowing employees to receive fiat wages while routing a portion of their pay into stablecoins like USDC or USDT. This model reduces regulatory friction for employers who must maintain traditional payroll systems for statutory deductions, while still offering employees crypto access. It is less suited for fully remote, crypto-native teams that prefer 100% on-chain settlement.

Provider Comparison

The following table compares the primary infrastructure options based on supported chains, compliance depth, and fee structures. These metrics reflect standard enterprise configurations as of 2026.

| Provider | Supported Chains | Compliance Focus | Fee Structure |

|---|---|---|---|

| Circle | Ethereum, Polygon, Solana, Arbitrum | Issuer-level reserve audits, KYC/AML for wallet providers | Network gas fees; no direct payroll processing fees |

| Rise | Ethereum, Polygon, Arbitrum, Optimism | 1099-NEC reporting, contractor KYC, audit trails | Per-payroll transaction fee; enterprise volume discounts |

| Toku | Ethereum, Polygon, Base | Global tax documentation, KYC/AML for employees/contractors | Monthly platform fee + per-payout fee |

| Bitwage | Ethereum, Bitcoin (via Lightning), USDC native | Traditional payroll tax integration, split-payment compliance | Per-transaction fee; optional fiat withdrawal fees |

Market Context

USDC’s price stability is central to its utility in payroll. While the token is pegged to the US dollar, minor deviations can occur during periods of high market volatility or liquidity stress. Monitoring the stablecoin’s market performance helps treasury teams anticipate settlement timing and potential slippage.

When evaluating providers, prioritize those with transparent reserve attestations and clear audit trails. Compliance is not optional in payroll; it is the primary risk vector. Choose a rail that aligns with your team’s geographic distribution and tax obligations.

Tax withholding and regulatory risks

Paying salaries in USDC introduces immediate tax complexity because the United States Internal Revenue Service (IRS) classifies virtual currency as property, not legal tender. This classification applies to USDC just as it does to Bitcoin or Ethereum. When an employer transfers USDC to an employee, the transaction is treated as a taxable event. The fair market value of the USDC at the moment of receipt determines the employee’s gross income for withholding purposes.

The employer’s withholding obligations remain unchanged in form but become more volatile in practice. You must calculate federal income tax, Social Security, and Medicare taxes based on the USDC’s fiat equivalent at the time of payment. If the value of USDC fluctuates between the payroll run date and the date you remit taxes to the IRS, the employer may face a shortfall or an overpayment. This mismatch creates a direct financial risk that does not exist with traditional fiat payroll.

Misclassification of workers compounds these risks. If a company pays a contractor in USDC but treats them as an employee for tax purposes, or vice versa, the entity risks penalties from both the IRS and state agencies. The method of payment does not alter the legal definition of the worker. Using USDC does not exempt the employer from standard employment law requirements.

Global teams add another layer of difficulty. While the US treats USDC as property, other jurisdictions may classify stablecoins differently. Some countries view crypto payments as barter transactions, while others have specific withholding rules for digital assets. Employers must verify the local tax treatment in every country where they pay staff. A strategy that works for US-based employees may violate tax codes in Europe or Asia.

Circle, the issuer of USDC, provides tools for businesses to manage transactions, but it does not provide tax advice. The responsibility for accurate withholding and reporting rests entirely with the employer. Relying on the stability of the peg to ignore tax timing issues is a dangerous oversight. The peg ensures the value remains near $1.00, but it does not eliminate the administrative burden of tracking fair market value for every payroll transaction.

Setting up compliant USDC payroll workflows

Implementing USDC payroll requires a structured approach to onboarding, funding, and execution. The process mirrors traditional payroll but introduces specific technical steps for wallet management and blockchain verification. Establishing these workflows ensures that payments are traceable, accurate, and compliant with regulatory standards.

Register with a payroll provider that supports USDC transactions. This account serves as the central hub for managing contractors, tracking payments, and generating compliance reports. Ensure the provider integrates with US-regulated financial institutions to maintain the 1:1 backing required for stablecoin stability.

Invite workers to the platform and collect their wallet addresses. Verify the network compatibility (e.g., Polygon, Ethereum) to avoid transaction failures. Assign a nickname to each wallet for internal tracking, but ensure the public address is accurately recorded to prevent misdirected funds.

Deposit fiat currency into your business account to purchase USDC. Most providers allow you to fund the account via bank transfer or credit card, which is then converted into USDC at a 1:1 ratio. This step ensures you have sufficient liquidity to cover payroll obligations before the payment cycle begins.

Initiate payments to the verified wallet addresses. The platform processes the transaction on the blockchain, providing a permanent, immutable record. Verify that the transaction hash is generated and that the recipient confirms receipt. This step finalizes the payroll cycle and creates an audit trail for tax and compliance purposes.

The operational integrity of USDC payroll depends on the accuracy of wallet addresses and the reliability of the underlying blockchain. By following these steps, organizations can maintain a compliant, efficient, and transparent payroll system.

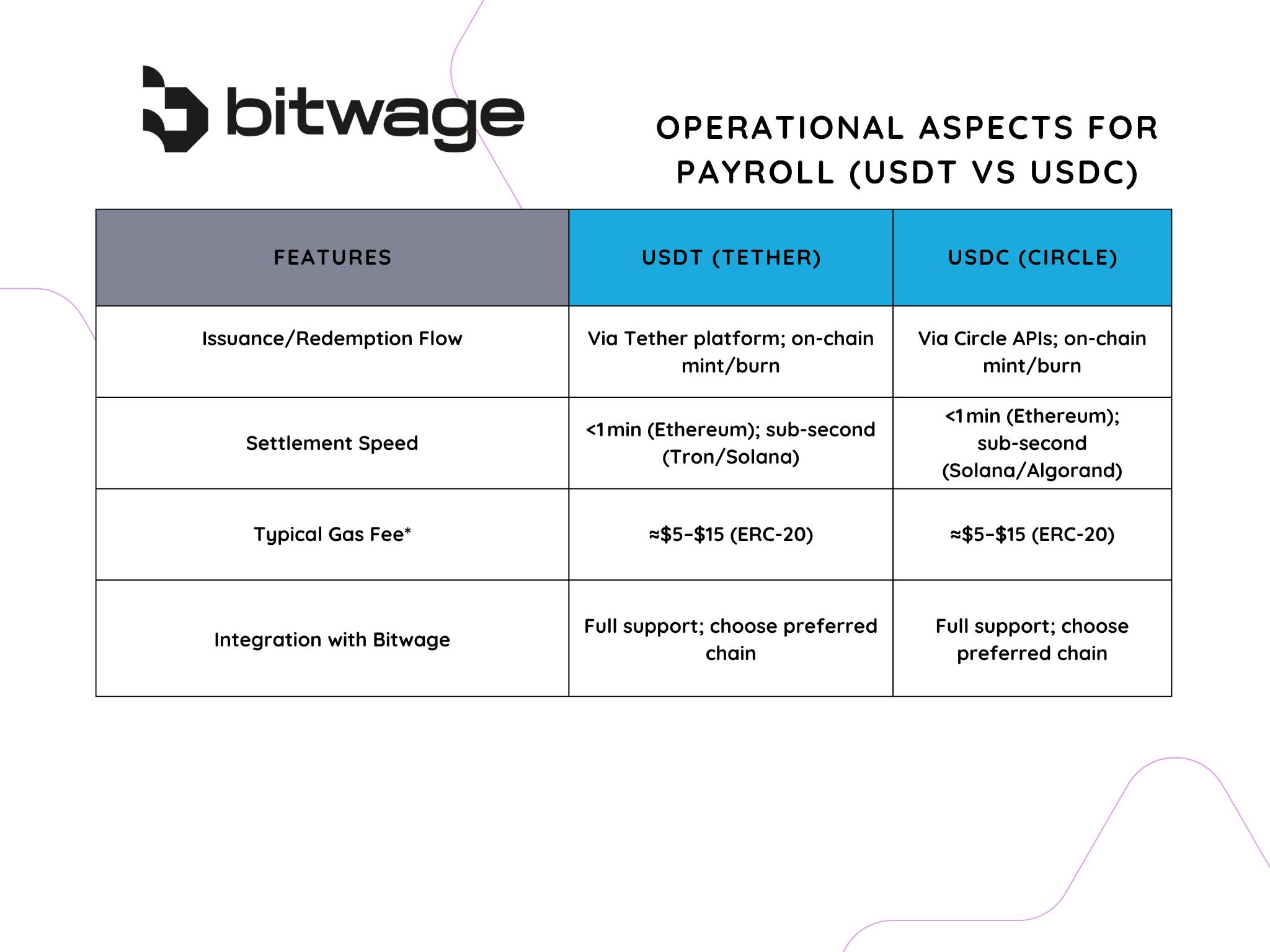

USDC vs USDT for corporate payroll

Choosing between USD Coin (USDC) and Tether (USDT) for payroll requires evaluating regulatory standing and reserve transparency over short-term liquidity. USDC is issued by Circle and backed by cash and short-dated U.S. Treasuries held in segregated accounts with U.S. regulated financial institutions. This structure aligns with strict compliance expectations and provides monthly attestation reports for auditability.

USDT is issued by Tether Limited and has historically faced scrutiny regarding the composition of its reserves. While it offers broader liquidity across exchanges, its regulatory framework operates with less transparency than USDC. For corporate payroll, where tax reporting and fund segregation are mandatory, USDC’s U.S.-centric regulatory alignment reduces legal exposure.

| Feature | USDC | USDT |

|---|---|---|

| Issuer | Circle | Tether Limited |

| Reserve Backing | Cash & U.S. Treasuries | Mixed (Cash, Treasuries, Commercial Paper) |

| Regulatory Status | U.S. Regulated (NYDFS) | Offshore (BVI), evolving U.S. compliance |

| Audit Frequency | Monthly Attestations | Quarterly Attestations |

The primary risk in payroll is stability. A regulatory action against an issuer or a reserve devaluation can halt payments. USDC’s transparent, U.S.-based reserve model offers a clearer path to compliance for finance teams managing employee obligations.

Frequently asked questions about USDC payroll

How does the IRS treat USDC payroll?

The IRS classifies virtual currency, including USDC, as property. When an employer pays an employee in USDC, it is a taxable event. The fair market value of the USDC at the time of receipt determines the employee’s gross income. Employers must withhold federal income tax, Social Security, and Medicare taxes based on the fiat equivalent of the USDC at that moment.

What are the tax risks of paying contractors in USDC?

Paying contractors in USDC triggers 1099-NEC reporting requirements if the contractor is a US person. The employer must report the fair market value of the USDC paid. If the value of USDC fluctuates between payment and tax remittance, the employer bears the risk of shortfall or overpayment. Additionally, misclassifying a contractor as an employee (or vice versa) while using crypto does not exempt the employer from standard employment law penalties.

Can USDC payroll be used for international teams?

Yes, but compliance requirements vary by jurisdiction. While the US treats USDC as property, other countries may classify stablecoins differently, potentially as barter or taxable income with specific withholding rules. Employers must verify local tax treatment in each country where staff are located. Some jurisdictions may require conversion to local fiat for statutory deductions, while others allow direct crypto settlement.

No comments yet. Be the first to share your thoughts!