Set up compliant USDC payroll

Choosing the right payroll provider is the first step in running USDC payroll. The right platform handles the technical conversion between stablecoins and fiat, ensuring you meet IRS reporting requirements while keeping your audit trail intact.

In 2026, USDC payroll has moved from experimental to essential for many global teams. It allows companies to bypass slow banking rails and reduce foreign exchange costs, while giving workers faster access to their earnings. However, not all providers offer the same level of compliance support. You need a vendor that can bridge the gap between blockchain transactions and traditional tax reporting.

Before integrating, confirm your provider is registered as a Money Services Business (MSB) with FinCEN. This registration is mandatory for any entity facilitating fiat conversions. It ensures the vendor adheres to federal anti-money laundering (AML) standards, which is a baseline requirement for compliant USDC payroll.

The IRS treats cryptocurrency payments as property, not currency. Your provider must automatically generate the necessary 1099 forms for contractors and employees, accurately reflecting the fair market value at the time of payment. Without this automated reporting, you risk non-compliance and potential penalties during an audit.

Run a small test transaction to verify how the platform handles the conversion from USDC to fiat. Check if the funds settle directly into your bank account or if employees receive stablecoins. Ensure the exchange rate used is transparent and that the settlement time aligns with your payroll schedule to avoid delays.

Connect your chosen provider to your current Human Resources Information System (HRIS). This integration automates data entry, reducing manual errors in employee records and payment amounts. A seamless connection ensures that new hires and offboarding processes are reflected immediately in your USDC payroll system.

Calculate withholding on stablecoin wages

The IRS treats stablecoins like USDC as property, not currency. This classification means every payroll transaction is a taxable event based on the fair market value at the exact moment of payment. You must calculate withholding using the dollar value of the USDC at that specific timestamp, not the value at month-end or year-end.

To stay compliant, your payroll system must capture the spot price of USDC against the US Dollar at the time of disbursement. Use a reliable, real-time oracle or exchange rate feed to determine this value. Once you have the USD equivalent, apply standard federal, state, and FICA withholding rates as you would for fiat wages.

Consider this: paying $1,000 in USDC is identical to paying $1,000 in cash for tax purposes. If the price of USDC fluctuates by even a few cents during the payroll window, that variance affects the taxable income reported to the employee and the withholding amount remitted to the IRS.

Before sending any stablecoin wages, verify your valuation source. The IRS expects a reasonable, consistent method for determining fair market value. Document the rate source and timestamp for every payroll run to withstand potential audits.

-

Determine USDC/USD spot price at payment timestamp

-

Calculate gross wages in USD using spot price

-

Apply standard federal, state, and FICA withholding rates

-

Record transaction hash and valuation source for audit trail

For detailed guidance on property transactions, refer to IRS Notice 2014-21.

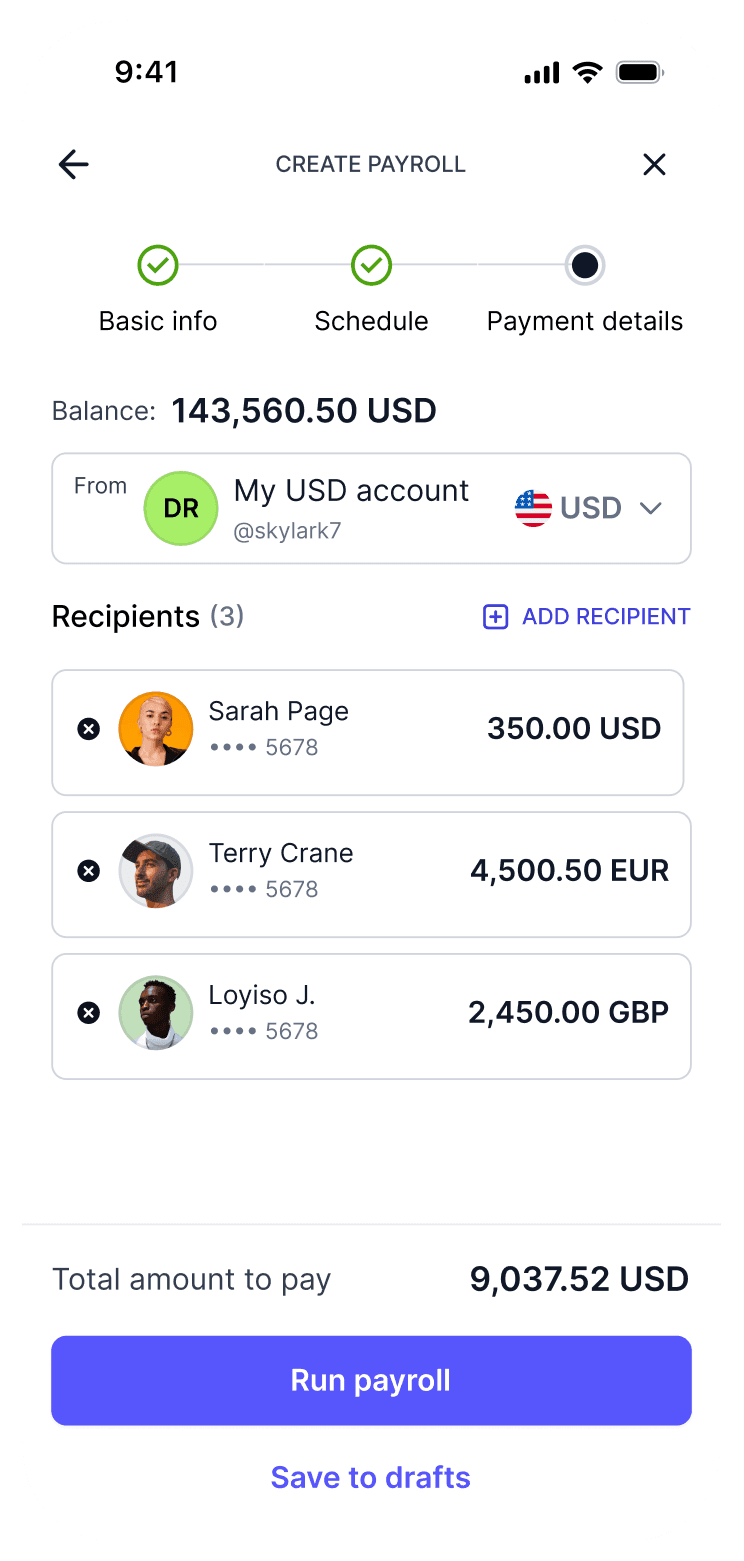

Execute the USDC payment transaction

Sending USDC for payroll requires precision because blockchain transfers are irreversible. Once the transaction hits the ledger, the funds are gone. To satisfy IRS reporting requirements, you must capture the transaction hash immediately, as this serves as the immutable proof of payment date and amount.

Use a dedicated corporate wallet or a compliant payroll platform to execute these transfers. Never use personal wallets for employee compensation, as this mingles personal and business assets, creating tax and liability complications.

Double-check every wallet address against your internal records. A single typo in a USDC address results in permanent loss of funds. If you are using a payroll platform, ensure the employee’s crypto wallet is verified and linked to their profile before initiating the batch.

USDC exists on multiple blockchains, including Ethereum, Solana, and Polygon. Ensure your payroll software and the recipient’s wallet support the same network. Sending USDC from an Ethereum-based system to a Solana-only wallet will fail or result in lost funds.

Enter the precise USDC amount owed for the pay period. If your payroll platform supports it, include a memo or reference field (e.g., "Payroll - Oct 2026") in the transaction note. This metadata helps both you and the employee reconcile the payment against their tax documents later.

On networks like Ethereum, gas fees can fluctuate significantly. Verify that the total deduction (wages + any platform fees) matches the agreed-upon compensation. Some platforms deduct fees from the employee’s payout, while others absorb them; clarify this policy beforehand to avoid disputes.

Once confirmed, submit the transaction. Immediately copy the transaction hash (TXID) from the confirmation screen. Save this hash in your payroll ledger alongside the fiat equivalent value on the date of transfer. This hash is your primary evidence for IRS audits regarding the timing and validity of the payment.

File IRS forms for digital asset wages

Paying staff and contractors in USDC does not change your tax reporting obligations. The IRS treats cryptocurrency as property, meaning every payment triggers a taxable event that must be documented on standard payroll forms. You must determine worker classification first, as this dictates which form you file and how the income is reported.

Contractors receiving $600 or more in USDC during the tax year require a Form 1099-NEC. You must report the fair market value of the stablecoins in USD at the exact moment of payment. Because stablecoins fluctuate, your payroll software must capture the USD conversion rate for each transaction. At year-end, aggregate these values and file the form with the IRS by January 31.

Employees paid in USDC receive a W-2 just like those paid in fiat. The USDC amount is converted to USD for payroll tax calculations, including Social Security and Medicare. You must withhold federal and state income taxes from the USD equivalent value before disbursing the tokens. The final W-2 shows the total USD wages subject to withholding, regardless of the crypto medium used for settlement.

| Feature | Independent Contractor | Employee |

|---|---|---|

| Form | 1099-NEC | W-2 |

| Tax Withholding | None required | Income, Social Security, Medicare |

| Reporting Threshold | $600+ per year | All wages subject to tax |

| Filing Deadline | January 31 | January 31 |

Avoid common payroll compliance errors

Stablecoin payroll simplifies cross-border payments, but it introduces specific reporting traps that can trigger IRS penalties or state regulatory flags. Most errors stem from treating digital assets like fiat currency without adjusting for their unique volatility and tracking requirements. The following pitfalls are the most common sources of non-compliance in 2026.

Failing to report full fair market value

The IRS treats cryptocurrency as property, not currency. When you pay an employee in USDC, you must report the fair market value (FMV) in USD on the date of the transaction, not the amount in stablecoins. Reporting only the token amount or an estimated value can lead to underreported wages and subsequent audits. Use a reliable oracle or exchange rate at the exact moment of payout to determine the correct W-2 or 1099 amount.

Mixing personal and business wallets

Using a personal wallet to send payroll USDC is a major red flag for both tax authorities and financial institutions. It commingles funds, making it nearly impossible to separate business expenses from personal assets. This practice obscures the audit trail and can pierce the corporate veil, exposing owners to personal liability. Always use a dedicated, business-registered wallet for payroll transactions to maintain clear financial boundaries.

Ignoring state-specific stablecoin regulations

Federal tax rules are just one part of the compliance picture. States like New York (BitLicense) and California have specific regulations regarding the issuance and transfer of stablecoins. Some states require additional money transmitter licenses or specific disclosures when paying wages in digital assets. Failing to check local laws can result in fines or the inability to legally process crypto payroll in that jurisdiction.

Overlooking transaction fee deductions

Gas fees and network transaction costs are business expenses, but they are often overlooked in payroll calculations. If the employee bears the transaction fee, it may be construed as a reduction in their wages, potentially violating minimum wage laws. Conversely, if the business pays the fee, it must be tracked separately as an operational expense to ensure accurate profit and loss reporting.

Usdc payroll compliance: what to check next

Managing USDC payroll requires understanding recent governance shifts and how the IRS treats digital assets. These changes directly impact how you report wages and withhold taxes.

Always verify the current list of supported networks on Circle’s official status page before processing payments. Using deprecated chains can result in lost funds and compliance failures.

No comments yet. Be the first to share your thoughts!