The USDC Payroll 2026 Market Shift

The landscape of global compensation is undergoing a structural reset in 2026. As organizations seek to bypass the friction of traditional cross-border banking, USDC payroll has emerged as the preferred instrument for international teams. This shift is not driven by speculative crypto trends, but by the demand for predictable, regulated, and programmable money. Companies are moving away from volatile digital assets toward stablecoins that maintain parity with the US dollar, ensuring that employee compensation remains stable from pay date to deposit.

Stablecoin payroll offers a distinct advantage in speed and cost efficiency. Traditional wire transfers often take days to clear and incur significant foreign exchange (FX) fees. In contrast, USDC transactions settle on-chain in minutes, regardless of geographic boundaries. This immediacy provides workers with faster access to their earnings, a critical factor for global talent retention. The technology effectively replaces slow, legacy rails with a modern, digital infrastructure that aligns with the pace of remote work.

Regulatory clarity has further cemented USDC’s position. Unlike decentralized cryptocurrencies, USDC is issued by a regulated financial infrastructure provider, offering the auditability and compliance features required by high-stakes corporate finance departments. This regulatory alignment reduces legal risk for employers while providing the technological benefits of blockchain. As 2026 progresses, the integration of USDC into smart contract automation is becoming standard practice for multinational corporations.

The stability of USDC against the US dollar is evident in its trading performance. The chart above demonstrates the coin’s tight peg to fiat currency, contrasting sharply with the volatility seen in other digital assets. This stability is essential for payroll, where employees expect their wages to hold their value between pay periods. The reliability of USDC makes it a practical tool for managing global payrolls without exposing companies or workers to unnecessary market risk.

How smart contracts automate payroll

Smart contracts automate the USDC payroll process by encoding payment logic directly into immutable code on the blockchain. Instead of manual bank transfers, the contract acts as a self-executing agreement that triggers transfers only when predefined conditions are met. This reduces administrative overhead and eliminates the delays inherent in traditional banking rails.

The execution flow begins with trigger conditions. For global teams, these triggers often align with specific dates or verified work milestones. In 2026, the calendar includes 27 biweekly pay periods, requiring precise scheduling logic to ensure compliance with labor laws across different jurisdictions. The contract checks for these temporal markers before initiating any transfer.

Currency conversion relies on oracles for accurate foreign exchange (FX) rates. Since USDC is a USD-pegged stablecoin, employees in other regions need real-time conversion data to determine their local purchasing power. Oracles fetch live FX data from trusted financial sources and feed it into the contract, ensuring that each payment reflects the current market rate at the moment of execution.

Tax withholding and compliance risks

Smart contract automation simplifies the mechanics of payment, but it does not absolve employers of statutory tax obligations. When you use USDC for payroll, the blockchain executes the transfer, yet it cannot interpret local withholding tables, social security caps, or income tax brackets. The legal distinction between paying an employee and paying an independent contractor remains the primary compliance trap. Misclassifying a worker to avoid withholding complexity can trigger severe penalties from the IRS and state agencies, regardless of how transparent the crypto transaction appears.

The 2026 payroll calendar introduces specific timing risks for global teams. Unlike traditional bank transfers, stablecoin settlements are instantaneous, but tax reporting deadlines are fixed. For example, 2026 contains 27 biweekly pay periods instead of the typical 26, a shift that affects Q1 and Q2 withholding calculations. If your smart contract releases funds on a fixed interval without adjusting for these calendar shifts, you may under-withhold or over-withhold, creating reconciliation nightmares during tax season. Government payroll calendars, such as those published by the GSA, serve as the baseline for understanding these periodic shifts, even if your team is distributed globally.

Reporting requirements vary significantly by jurisdiction. In the United States, crypto payments are treated as property for tax purposes, meaning each distribution may have a taxable event component separate from the wage income. Employers must still issue Form W-2 for employees and Form 1099-NEC for contractors. The challenge lies in valuing the USDC at the moment of transfer to determine the fair market value for reporting. Without integrated payroll software that captures the exact exchange rate at the time of the smart contract execution, your accounting records will likely be inaccurate.

For international teams, the complexity multiplies. Some countries require tax withholding in local fiat currency, while others allow crypto payments with specific reporting. You must determine if the USDC payment constitutes "wages" under local labor laws or if it is a B2B service contract. This classification dictates whether you need to register as an employer in that jurisdiction. Relying on a smart contract to handle cross-border compliance is legally insufficient; you need a human-reviewed payroll framework that sits above the code.

Leading USDC Payroll Platforms Compared

Selecting a USDC payroll provider requires evaluating technical infrastructure against regulatory obligations. In 2026, the market distinguishes itself through multi-chain capabilities and automated tax withholding. The following comparison highlights three primary platforms: Eco, Bitwage, and Rise.

Eco provides robust multi-chain support, enabling payments across Ethereum, Solana, and Polygon. Bitwage focuses heavily on compliance, offering direct integration with traditional tax filing systems. Rise emphasizes low transaction fees and stablecoin-specific payroll logic. All three support USDC, but their approaches to risk management and user experience differ significantly.

| Feature | Eco | Bitwage | Rise |

|---|---|---|---|

| Supported Chains | Multi-chain (ETH, SOL, POL) | Ethereum (ERC-20) | Multi-chain (ETH, POL) |

| Tax Withholding | Automated via partners | Direct IRS integration | Manual/External tools |

| Compliance | SOC 2 Type II | FINRA Registered | KYC/AML Verified |

| Fee Structure | Tiered subscription | Per-payee fee | Low flat fee |

Technical infrastructure dictates reliability. USDC price stability is critical for payroll accuracy. Monitor current market conditions using provider-backed widgets to ensure audit compliance.

For deeper technical analysis, track USDC liquidity and volume trends. This data supports informed decisions regarding treasury management and payment timing.

Implementation checklist for 2026

Deploying USDC payroll requires rigorous alignment between technical execution and regulatory compliance. Before automating payments, verify that your legal entity is registered in a jurisdiction that recognizes stablecoin transactions for salary disbursement. Consult local tax authorities to confirm withholding requirements and reporting obligations for digital asset wages. Failure to classify these payments correctly can trigger significant penalties.

Select a payroll platform capable of handling USDC transfers and automatic tax withholding. The system must support the 27 biweekly pay periods in 2026, ensuring accurate calendar alignment. Evaluate platforms based on their ability to generate compliant tax forms (such as 1099s or W-2s) and their security protocols for private key management.

Configure tax rules and employee communication protocols. Establish clear guidelines for employees regarding wallet security and the tax implications of receiving stablecoins. Provide training on how to convert USDC to fiat currency if desired, and document the exchange rate mechanism used at the time of payment to ensure fair valuation.

Confirm your business structure allows for digital asset payroll. Review local regulations in each employee's jurisdiction to ensure compliance with labor laws and tax reporting standards for stablecoin wages.

Choose a platform that supports USDC transfers and integrates with your existing HR systems. Prioritize providers with strong security audits and clear fee structures for transaction processing and currency conversion.

Set up automated withholding for income tax, social security, and other statutory deductions. Ensure the platform can generate accurate tax documentation for both the employer and employees, reflecting the fair market value of USDC at the time of payment.

Run a pilot program with a small group of employees or contractors. Verify that transactions settle correctly, tax calculations are accurate, and employees can successfully receive and access their funds. Resolve any issues before full-scale deployment.

Communicate the new payroll method clearly. Provide employees with instructions on setting up digital wallets, understanding the tax implications, and converting USDC to fiat if needed. Offer ongoing support to address questions and ensure a smooth transition.

The transition to USDC payroll offers significant efficiency gains, but it demands careful planning. By following this checklist, you can mitigate risks and ensure a compliant, smooth implementation for your global team.

USDC payroll 2026 FAQ

Addressing specific operational and compliance questions regarding the transition to stablecoin payroll structures in 2026.

How many biweekly payrolls occur in 2026?

2026 contains 27 biweekly pay periods rather than the typical 26. This anomaly occurs because the year begins on a Thursday, pushing the final pay period into January 2027. For automation systems, this requires explicit handling of the extra distribution cycle to ensure accurate fiscal year reporting and contract alignment.

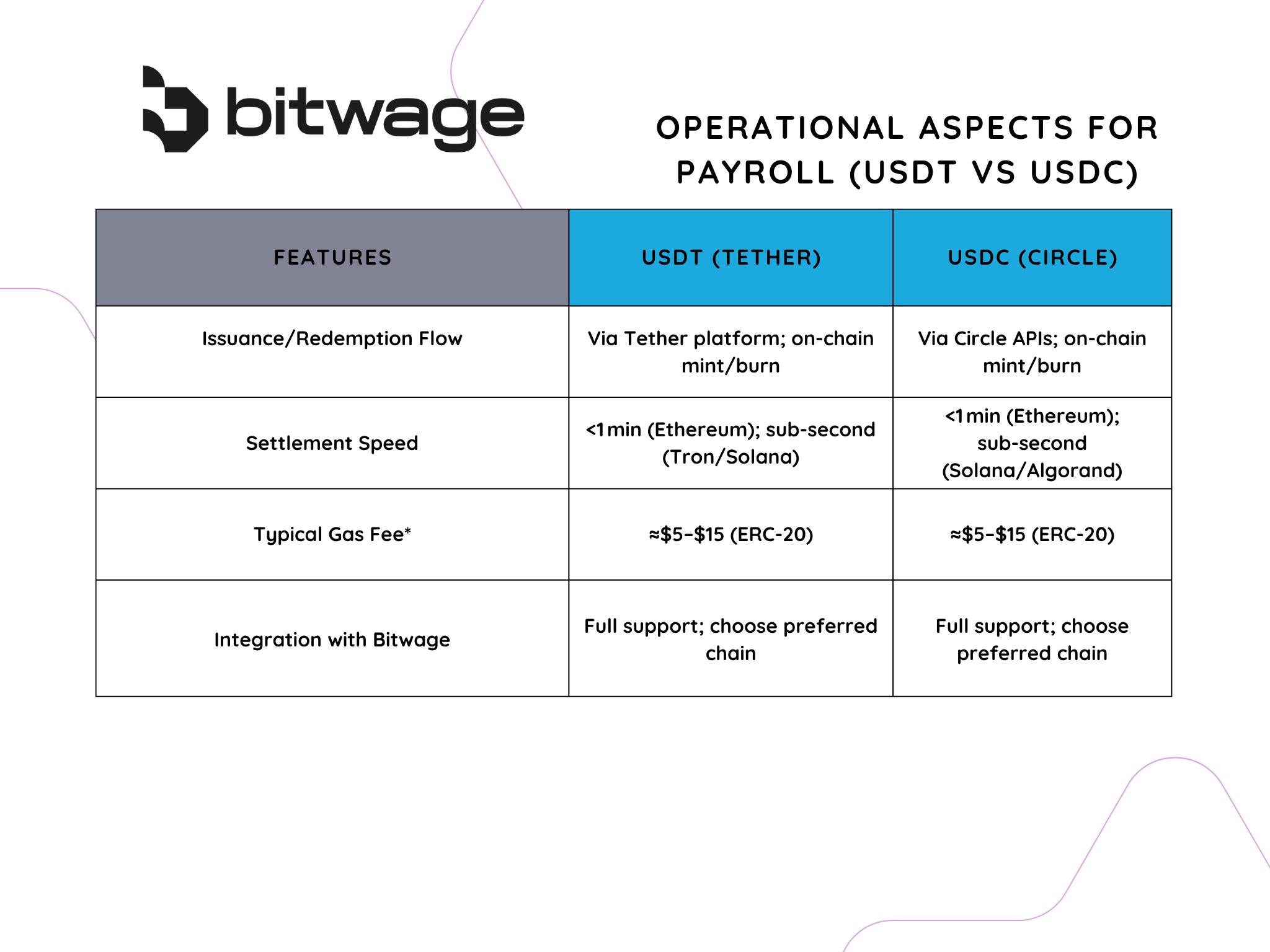

Is USDC or USDT better for payroll?

USDC is generally preferred for payroll due to its regulatory transparency and reserve structure. Circle publishes monthly attestation reports, providing a higher degree of auditability required for HR and finance teams. USDT, while widely used for trading, operates with different compliance frameworks that may introduce additional due diligence burdens for corporate payrolls.

How does smart contract automation handle tax withholding?

Smart contracts can automate gross disbursement, but tax withholding remains a legal obligation of the employer. Integration with payroll providers is necessary to calculate federal, state, and local deductions before conversion. The contract should distribute the net USDC amount to the employee, while the employer retains the tax portion for quarterly filings.

What is the volatility risk of holding USDC for payroll?

USDC is pegged to the US dollar, minimizing volatility compared to Bitcoin or Ethereum. However, de-pegging events are a theoretical risk. Mitigation strategies include holding payroll funds in short-term Treasury bills via regulated issuers or maintaining a small buffer in fiat currency to cover immediate operational needs during market stress.

No comments yet. Be the first to share your thoughts!