Why USDC payroll compliance matters now

The regulatory landscape for digital asset compensation is tightening significantly as stablecoin adoption accelerates. In 2024, the use of stablecoins for payroll tripled from 3% in 2023 to 9.6%, with USDC accounting for 63% of all crypto payrolls

Under current IRS guidance, stablecoins are treated as property for tax purposes. This classification means that every payroll transaction—whether paying a salary or a contractor—can trigger a taxable event if the asset’s value fluctuates between the time it is earned and the time it is settled or converted. For employers, this creates a complex reporting burden involving Form 1099-NEC for contractors and standard wage withholding requirements for employees. Failure to accurately report these transactions can result in significant penalties.

Circle, the issuer of USDC, operates as a regulated financial service business under strict U.S. laws src-serp-5. While this regulatory framework provides transparency through monthly attestations of reserves, it does not exempt employers from federal tax compliance obligations. The convergence of widespread adoption and rigorous enforcement means that organizations adopting USDC payroll must prioritize compliance infrastructure to avoid legal and financial exposure.

IRS tax treatment of stablecoin payouts

Employers and employees must treat USDC as property, not currency, for federal tax purposes. The IRS guidance issued in 2019 established that digital assets with stable value, like USDC, are subject to the same tax rules as other property. This classification creates specific compliance obligations that differ significantly from traditional fiat payroll.

For employers, paying wages in USDC triggers the same withholding requirements as paying in dollars. You must calculate and remit federal income tax, Social Security, and Medicare taxes based on the fair market value of the USDC at the time of payment. This valuation is critical because the tax liability is fixed at the moment of transfer, regardless of how the employee later disposes of the asset.

Employees face capital gains or losses when they convert USDC to fiat or spend it. Because USDC is property, receiving it is not a taxable event in itself. However, if the USDC de-pegs or if the employee sells it after receiving it, any change in value since receipt is taxable. This means payroll teams must provide clear documentation of the fair market value at payment to help employees calculate their tax obligations accurately.

Comparing USDC payroll providers and tools

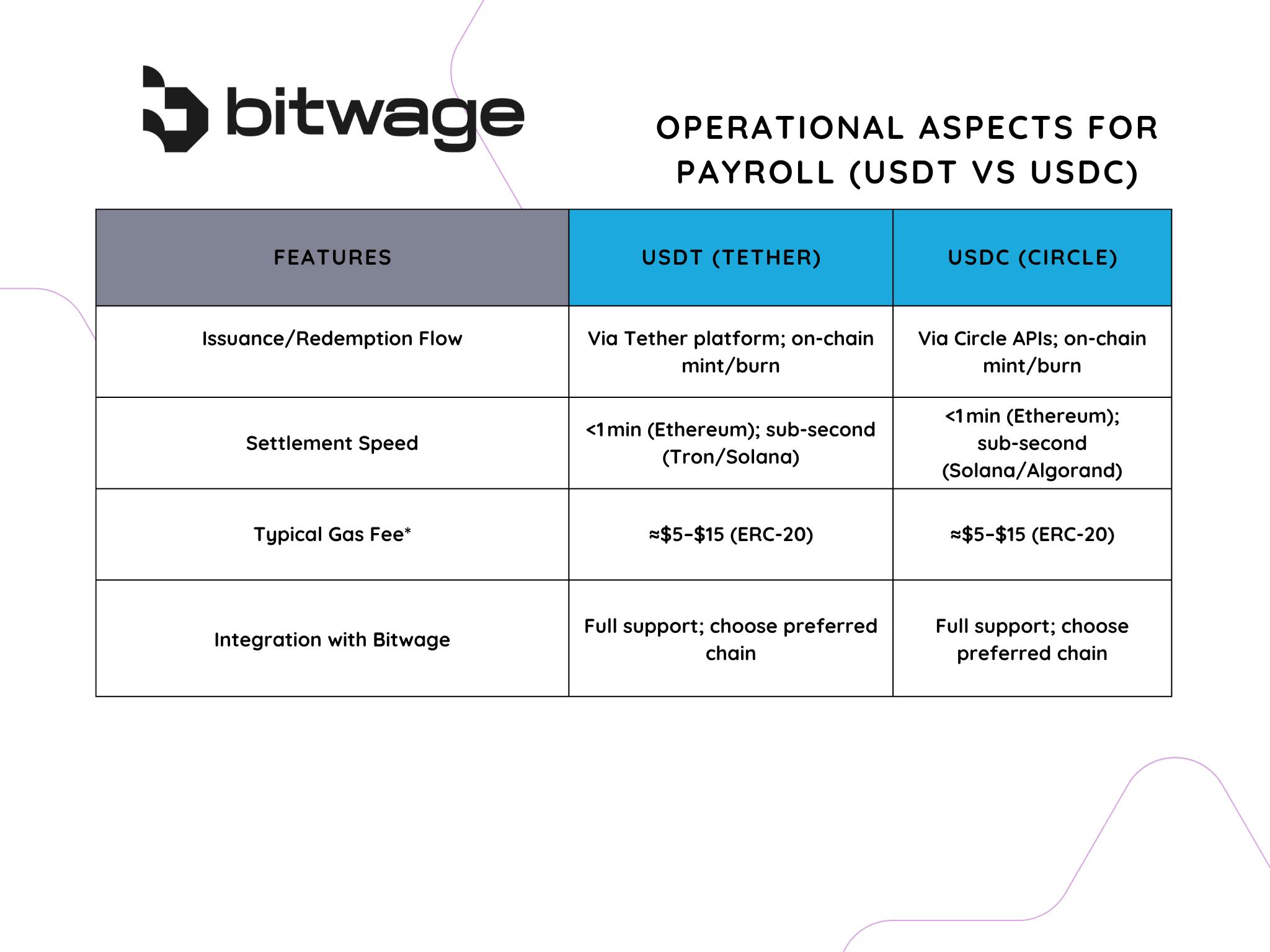

Selecting a payroll platform for stablecoin compensation requires evaluating how each vendor handles regulatory reporting, fiat conversion, and cross-border compliance. While Circle issues USDC, the infrastructure layer—how funds move from employer to employee—varies significantly by provider. The following comparison outlines the primary differences between Deel, Toku, Rise, and Multiplier to aid in compliance due diligence.

| Provider | Compliance & Reporting | Supported Regions | Fee Structure | USDC Integration Depth |

|---|---|---|---|---|

| Deel | Global tax forms (W-8/W-9, 1099), automated withholding in select jurisdictions | 150+ countries | Platform fee + payment processing fees; USDC funding may incur blockchain network fees | Direct funding via Coinbase; auto-conversion to fiat or stablecoin payout available |

| Toku | Built-in KYC/AML, 1099-NEC generation, audit trails for crypto transactions | Global, with emphasis on US and EU contractors | Percentage-based transaction fee; no separate platform fee for basic plans | Native USDC support; holds funds in regulated custodial wallets before payout |

| Rise | IRS-compliant reporting, contractor onboarding verification, automated tax document generation | Global, strong presence in North America and Europe | Flat fee per payment or monthly subscription; USDC conversion fees apply | Direct USDC payouts to personal wallets; supports hybrid fiat/crypto payments |

| Multiplier | Contractor verification, tax form generation, compliance checks for restricted countries | 150+ countries, with localized entity options for EOR services | Per-contractor monthly fee or per-payment fee; USDC payouts may involve third-party conversion costs | USDC payout option for contractors; requires contractor wallet address and security verification |

Deel and Multiplier offer extensive global reach with established EOR (Employer of Record) capabilities, making them suitable for companies managing full-time employees alongside contractors. Deel’s integration with Coinbase allows for direct USDC funding, which can reduce friction for treasury management. Toku and Rise are built specifically for crypto-native workflows, offering deeper native support for stablecoin payouts without mandatory fiat conversion, though this requires careful attention to local tax reporting obligations.

When evaluating these tools, prioritize providers that generate automated 1099-NEC or local tax forms. The IRS treats cryptocurrency payments as property, meaning employers must report fair market value at the time of payment. Platforms that automate this calculation and reporting reduce the risk of compliance errors. Always verify that the provider’s terms of service explicitly state their role in tax reporting, as some act merely as payment facilitators rather than compliance partners.

Technical Risks and Settlement Delays

Processing payroll in USDC introduces distinct technical variables that differ from traditional fiat rails. While the underlying blockchain technology offers near-instant settlement, the actual arrival of funds depends on network congestion, gas fees, and the specific blockchain network used. For high-volume payroll runs, these micro-delays can compound, creating administrative friction if not properly accounted for in payroll schedules.

Network fees, or "gas," fluctuate based on blockchain demand. During peak usage, transaction costs can rise significantly, eroding the cost-saving benefits of stablecoin payroll. Employers must monitor these fees closely, particularly when processing payments across different networks such as Ethereum, Solana, or Polygon. Choosing a network with lower fees but sufficient liquidity is essential for maintaining predictable payroll costs.

Settlement finality is another critical factor. Unlike bank transfers that may take one to three business days, USDC transactions settle in seconds to minutes. However, this speed requires robust technical infrastructure. Payroll systems must be configured to detect confirmations accurately to avoid double-spending risks or premature payout recognition. Delays in confirmation can lead to discrepancies between the payroll ledger and the employee's wallet balance.

The reliability of USDC hinges on its issuer. Circle, as a regulated financial service provider, ensures that USDC is backed by cash and short-dated U.S. Treasuries held in regulated institutions. This regulatory compliance reduces the risk of de-pegging, a scenario where the stablecoin's value diverges significantly from $1.00. Using a regulated issuer like Circle provides a layer of financial stability that unregulated stablecoins cannot offer, protecting both the employer and the employee from sudden value fluctuations.

To visualize the stability of USDC against the US dollar, observe the technical chart below. This data demonstrates the tight peg that makes USDC suitable for payroll, where value predictability is paramount.

Audit your USDC payroll workflow

Before processing payments, finance and legal teams must verify that the underlying infrastructure meets 2026 regulatory standards. This audit ensures that USDC payroll operations remain compliant with tax withholding requirements and anti-money laundering (AML) protocols.

Confirm that the USDC issuer maintains current regulatory licenses and provides transparent monthly attestations. Ensure reserves are held in regulated U.S. financial institutions to mitigate counterparty risk.

Validate that your payroll platform can accurately calculate and remit federal, state, and local taxes. The system must support automated withholding for both W-2 employees and 1099 contractors to avoid IRS penalties.

Review the security architecture of the wallets used for payroll disbursement. Ensure multi-signature requirements are active and that private keys are stored in institutional-grade custody solutions to prevent unauthorized access.

Verify that all recipients have undergone rigorous Know Your Customer (KYC) checks. The payroll provider must maintain audit trails for all transactions to satisfy FinCEN reporting requirements.

Frequently Asked Questions About USDC Payroll

Is it safe to get paid in USDC?

USDC is a fiat-backed stablecoin issued by Circle, meaning every unit is backed 100% by cash and short-dated U.S. Treasuries held in regulated U.S. financial institutions [1]. The asset undergoes transparent monthly attestations to verify reserve integrity, providing a level of transparency and security distinct from unbacked cryptocurrencies. This structure makes it a compliant choice for payroll compared to volatile digital assets.

What crypto is used for payroll?

USDC is the standard cryptocurrency for payroll because of its stability. While some platforms support ETH or BTC, these are generally unsuitable for regular wage distribution due to price volatility. Most organizations use USDC either as a full salary replacement or as part of a hybrid model where the stablecoin portion is immediately converted to fiat upon receipt to mitigate market risk.

How is USDC payroll taxed?

The IRS treats cryptocurrency, including USDC, as property [2]. This means receiving USDC is a taxable event based on the fair market value at the time of receipt. Employers must withhold standard payroll taxes (Social Security, Medicare, and income tax) just as they would with fiat currency. Failure to report these transactions can lead to significant penalties for both the employee and the employer.

No comments yet. Be the first to share your thoughts!