The USDC payroll market overview

USDC payroll has transitioned from experimental adoption to a regulated infrastructure layer for global compensation. By 2026, the primary use case is no longer speculation but operational efficiency. Companies use USDC to settle payroll in near-instant time, bypassing the multi-day delays and high fees associated with traditional cross-border wire transfers. This shift is driven by the need to reduce friction for remote teams and independent contractors across international borders.

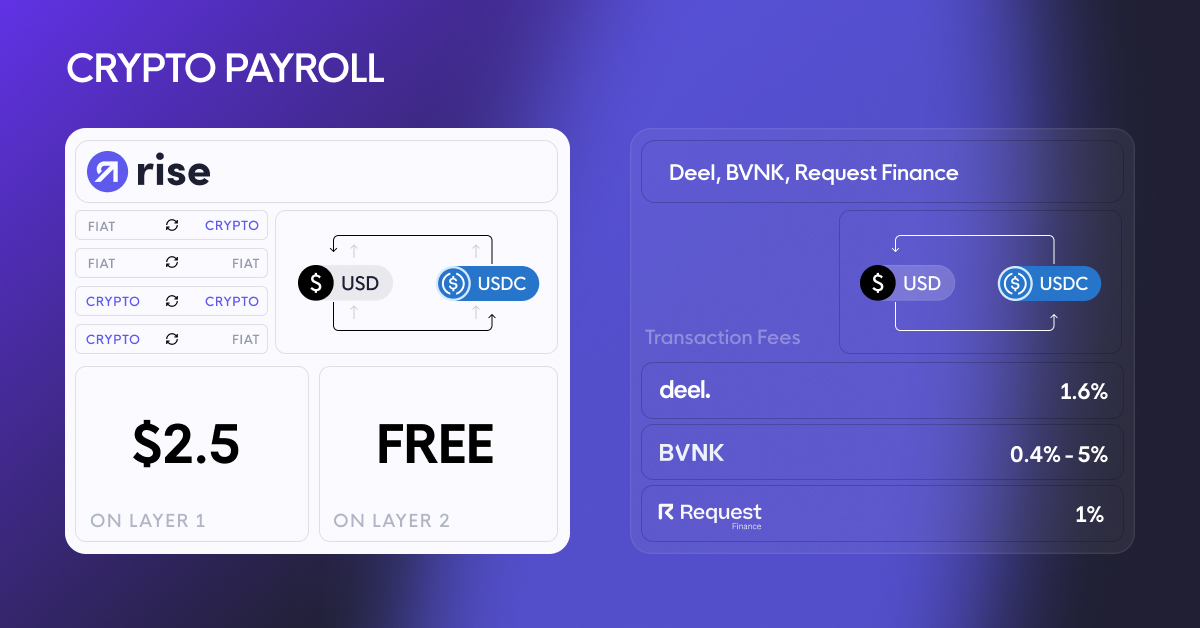

The market is anchored by Circle, the issuer of USDC, which provides the regulated stablecoin infrastructure. Unlike volatile cryptocurrencies, USDC is pegged 1:1 to the US dollar and backed by cash and short-term US treasuries, offering the price stability required for payroll. Major platforms like Deel, Rise, and Stripe have integrated USDC funding and payout options, allowing businesses to hold funds in stablecoins and disburse them directly to employees or contractors.

The operational reality of USDC payroll involves a specific compliance and cost structure. While the underlying blockchain transactions are fast, the legal framework remains tethered to traditional financial regulations. Businesses must ensure that payroll processing adheres to IRS reporting requirements for digital assets and local labor laws in the jurisdictions where employees reside. The cost advantage is clear: eliminating intermediary banks and foreign exchange markups reduces transaction costs to fractions of a cent per transfer.

This analysis focuses on the practical implications of using USDC for payroll. We examine the regulatory obligations, the actual cost savings compared to fiat rails, and the operational steps required to maintain compliance. The goal is to provide a clear picture of how USDC fits into the modern payroll stack, balancing speed and cost against legal and administrative responsibilities.

USDC tax withholding and reporting rules

Treating USDC as property rather than currency fundamentally changes how employers handle payroll taxes. Under IRS Notice 2014-21, virtual currency is classified as property for federal tax purposes. This classification means that receiving USDC as wages triggers a taxable event at the moment of receipt, regardless of whether the employee converts the tokens to fiat currency or holds them in a digital wallet.

Employers must calculate the fair market value of the USDC paid on the date the funds are made available to the employee. This value serves as the basis for withholding income taxes and Social Security and Medicare taxes. Just as with a traditional bank transfer, the payroll system must capture the precise USD equivalent at the time of payout to ensure accurate withholding calculations.

Reporting requirements mirror those for fiat payments. Employers must include the USD value of the USDC wages on Form W-2 for employees and Form 1099-NEC for independent contractors. The IRS requires that these forms reflect the dollar amount subject to withholding, not the quantity of tokens transferred. Failure to accurately report the fair market value can lead to significant compliance penalties for both the employer and the employee.

Payroll providers facilitating USDC payments, such as Deel or Rise, often integrate tools to help calculate these values. However, the ultimate legal responsibility for accurate withholding and reporting rests with the employer. Organizations must ensure their internal controls capture the timestamp and exchange rate data for every USDC transaction to defend against potential audits.

Platform comparison for USDC payouts

Use this section to make the USDC Payroll decision easier to compare in real life, not just on paper. Start with the reader's actual constraint, then separate must-have requirements from details that are merely nice to have. A practical choice should survive normal use, maintenance, timing, and budget. If a recommendation only works in an ideal situation, call that out plainly and give the reader a fallback path.

| Factor | What to check | Why it matters |

|---|---|---|

| Fit | Match the option to the primary use case. | A good deal still fails if it does not fit the job. |

| Condition | Verify age, wear, and service history. | Hidden condition issues erase upfront savings. |

| Cost | Compare purchase price with likely upkeep. | The cheapest option is not always the lowest-cost option. |

Network costs and settlement speed

Use this section to make the USDC Payroll decision easier to compare in real life, not just on paper. Start with the reader's actual constraint, then separate must-have requirements from details that are merely nice to have. A practical choice should survive normal use, maintenance, timing, and budget. If a recommendation only works in an ideal situation, call that out plainly and give the reader a fallback path.

The simplest way to use this section is to write down the must-have criteria first, then compare each option against those criteria before weighing nice-to-have features.

Compliance checklist for implementation

USDC Payroll works best as a clear sequence: define the constraint, compare the realistic options, test the tradeoff, and choose the path with the fewest hidden costs. That order keeps the advice usable instead of decorative. After each step, pause long enough to check whether the recommendation still fits the reader's actual situation. If it depends on perfect timing, unusual access, or a best-case budget, include a simpler fallback.

No comments yet. Be the first to share your thoughts!